Featured plate · Macro ·

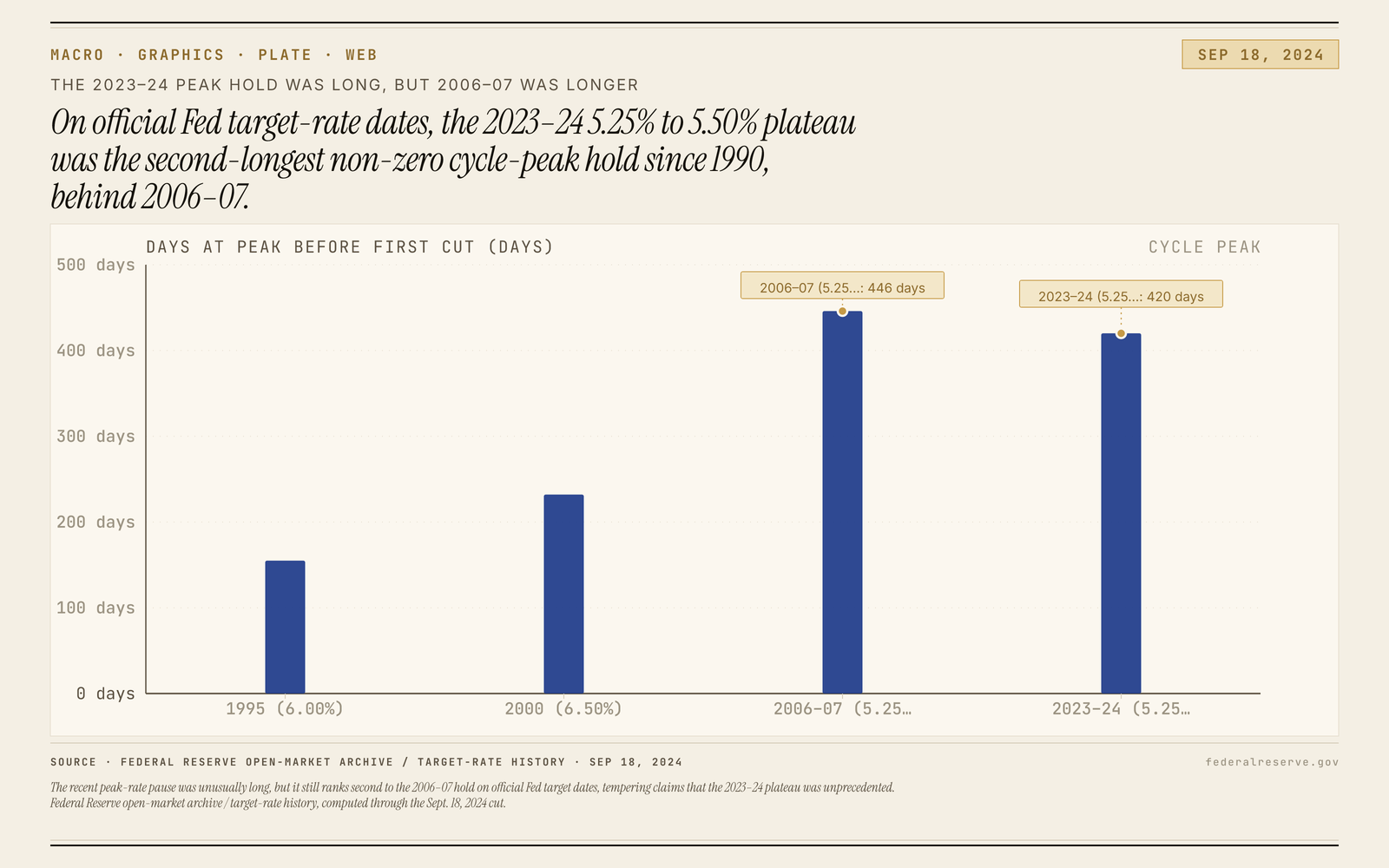

Fed timeline: 5.25%-5.50% ranks second

A pause at the top can look unprecedented until each peak is measured on the Fed’s own target-rate dates.

- Plate 11

Fed timeline: 5.25%-5.50% ranks second

A pause at the top can look unprecedented until each peak is measured on the Fed’s own target-rate dates.

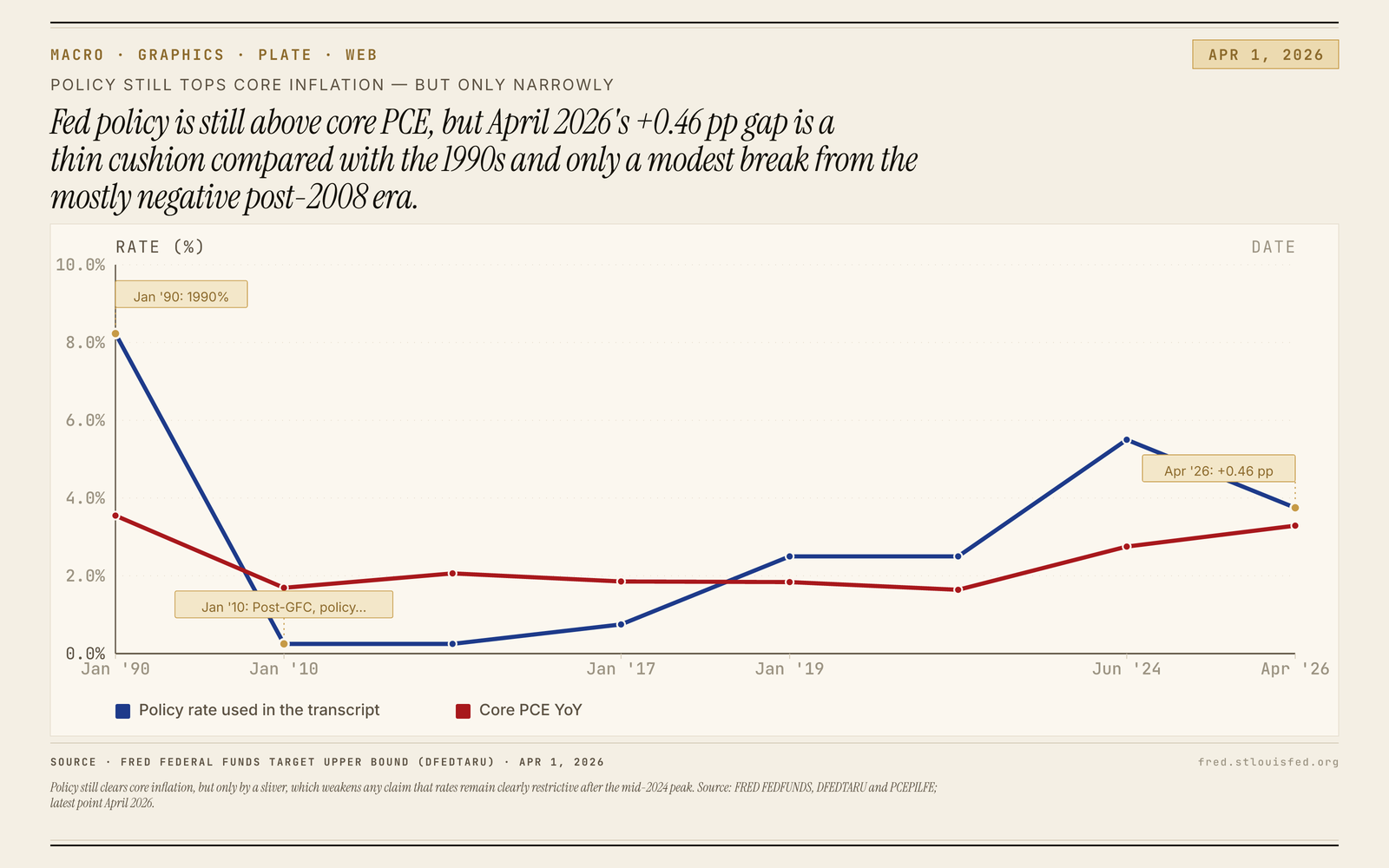

Plate 10

Plate 10Policy Rate Barely Tops Core PCE

The chart shows the policy rate still above core PCE by +0.46 pp.

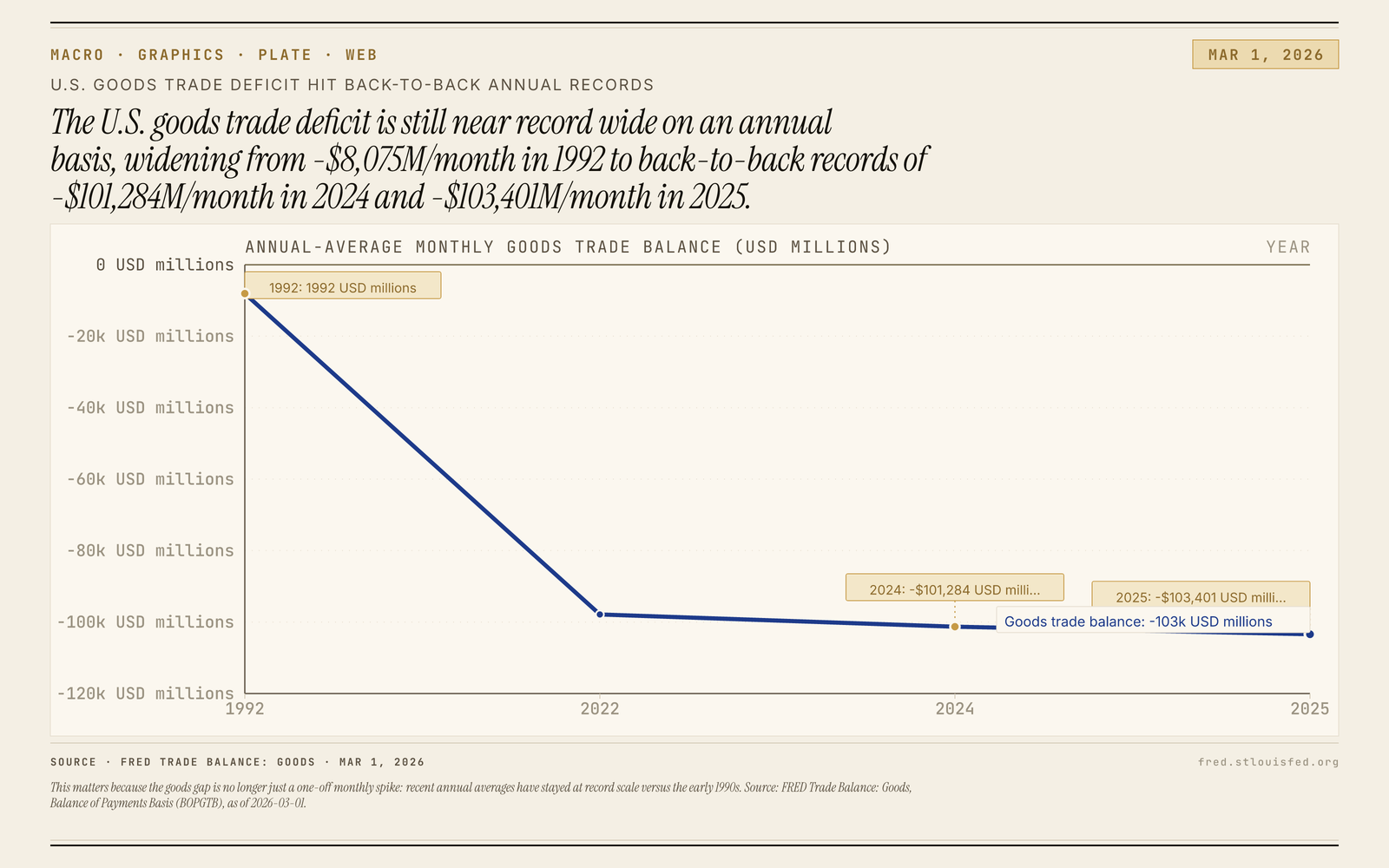

Plate 09

Plate 09Goods deficit near annual records

This chart shows the U.S.

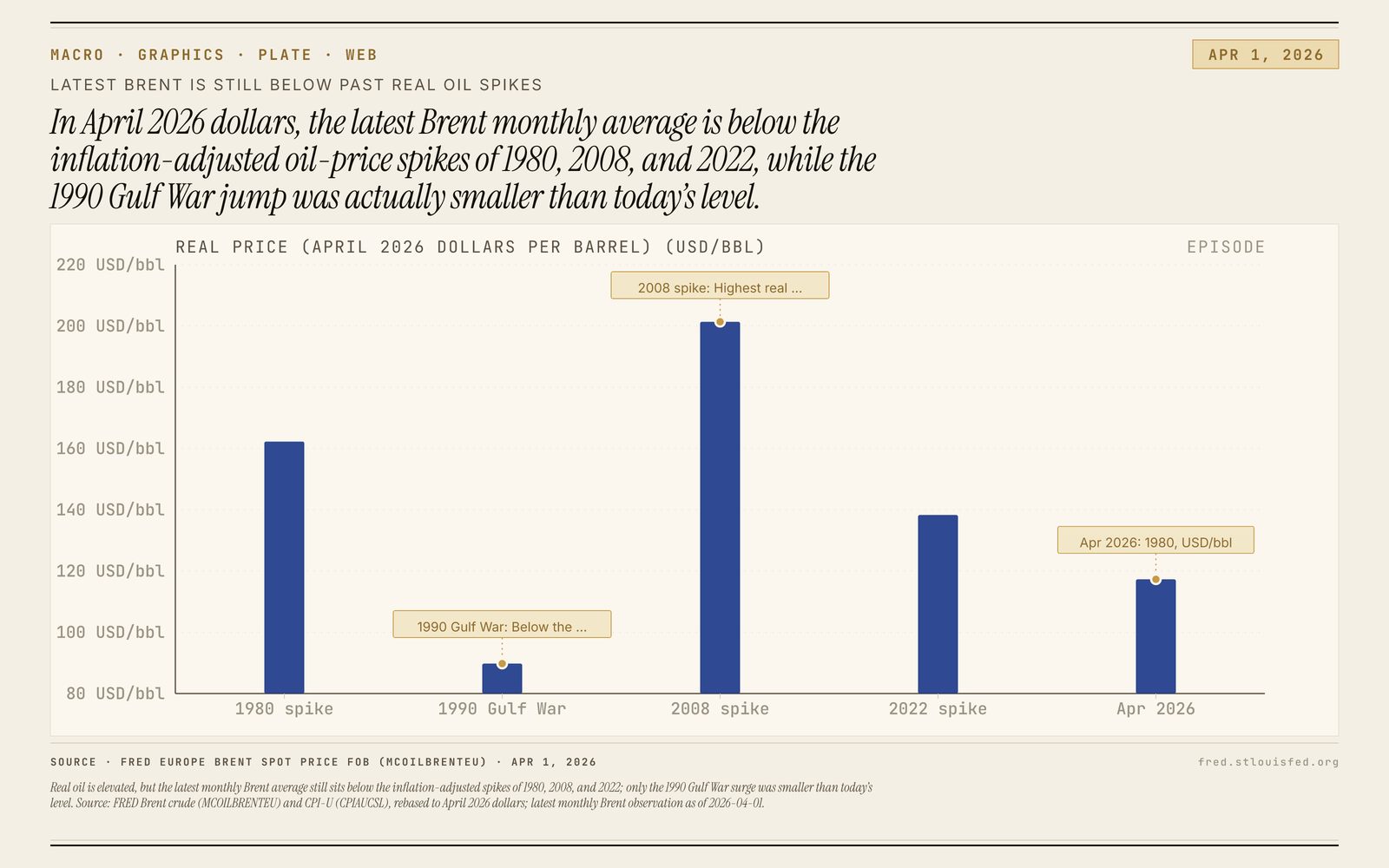

Plate 08

Plate 08Real Brent Below Prior Oil Shock Peaks

This chart puts selected oil shocks on the same constant-dollar yardstick, comparing the latest Brent monthly average with earlier crisis episodes rather than live spot headlines.

Plate 07

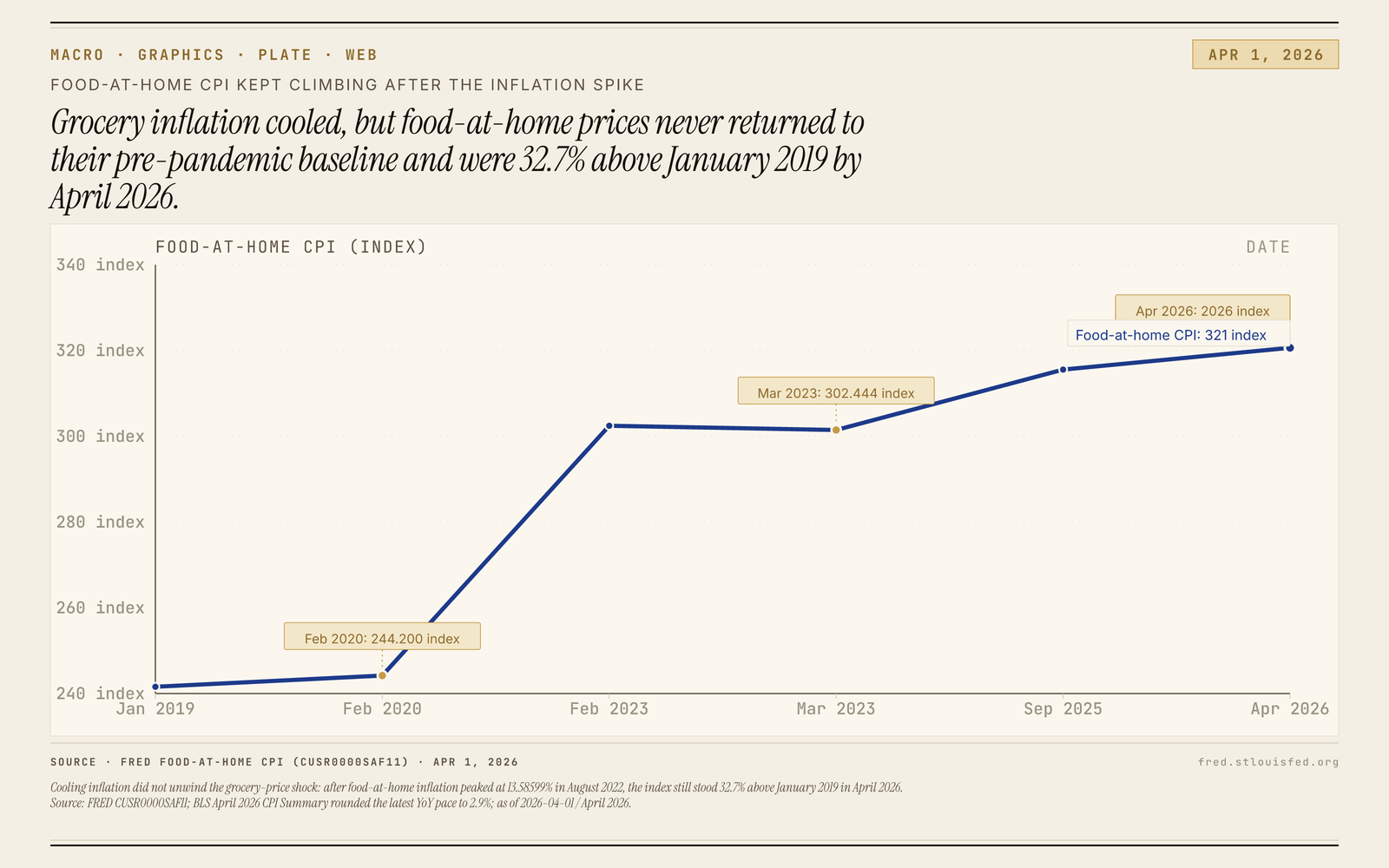

Plate 07Grocery inflation cooled. Prices stayed high.

This chart shows grocery prices staying high even after inflation cooled: the food-at-home CPI rose from 244.200 before the pandemic to 320.633, and the brief dip from 302.444 to 301.467 did not last (fred.stlouisfed.org).

Plate 06

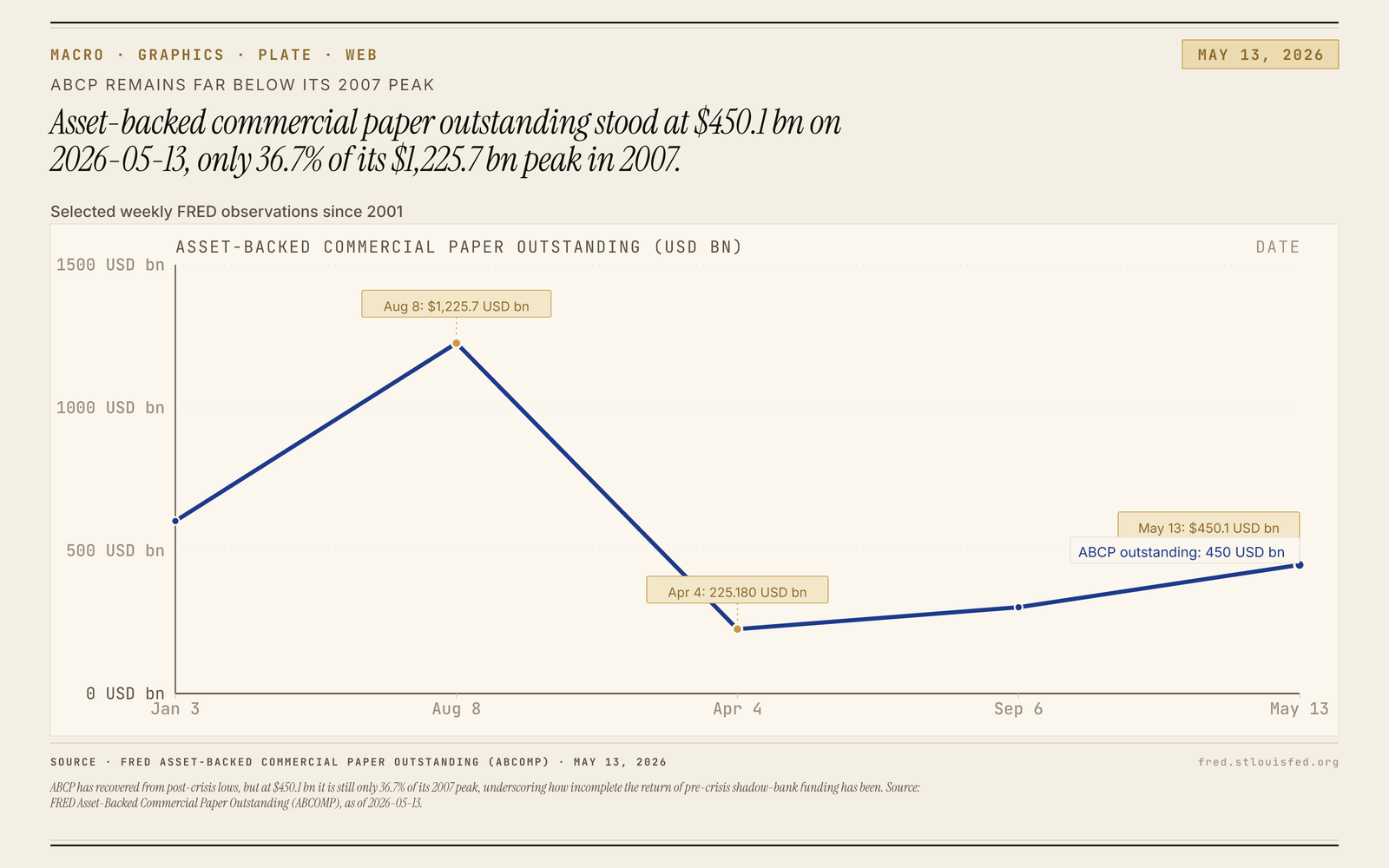

Plate 06ABCP is still just 36.7% of peak

This chart shows asset-backed commercial paper outstanding at $450.1 bn, only 36.7% of its $1,225.7 bn peak, according to FRED’s Asset-Backed Commercial Paper Outstanding series (fred.stlouisfed.org).

Plate 05

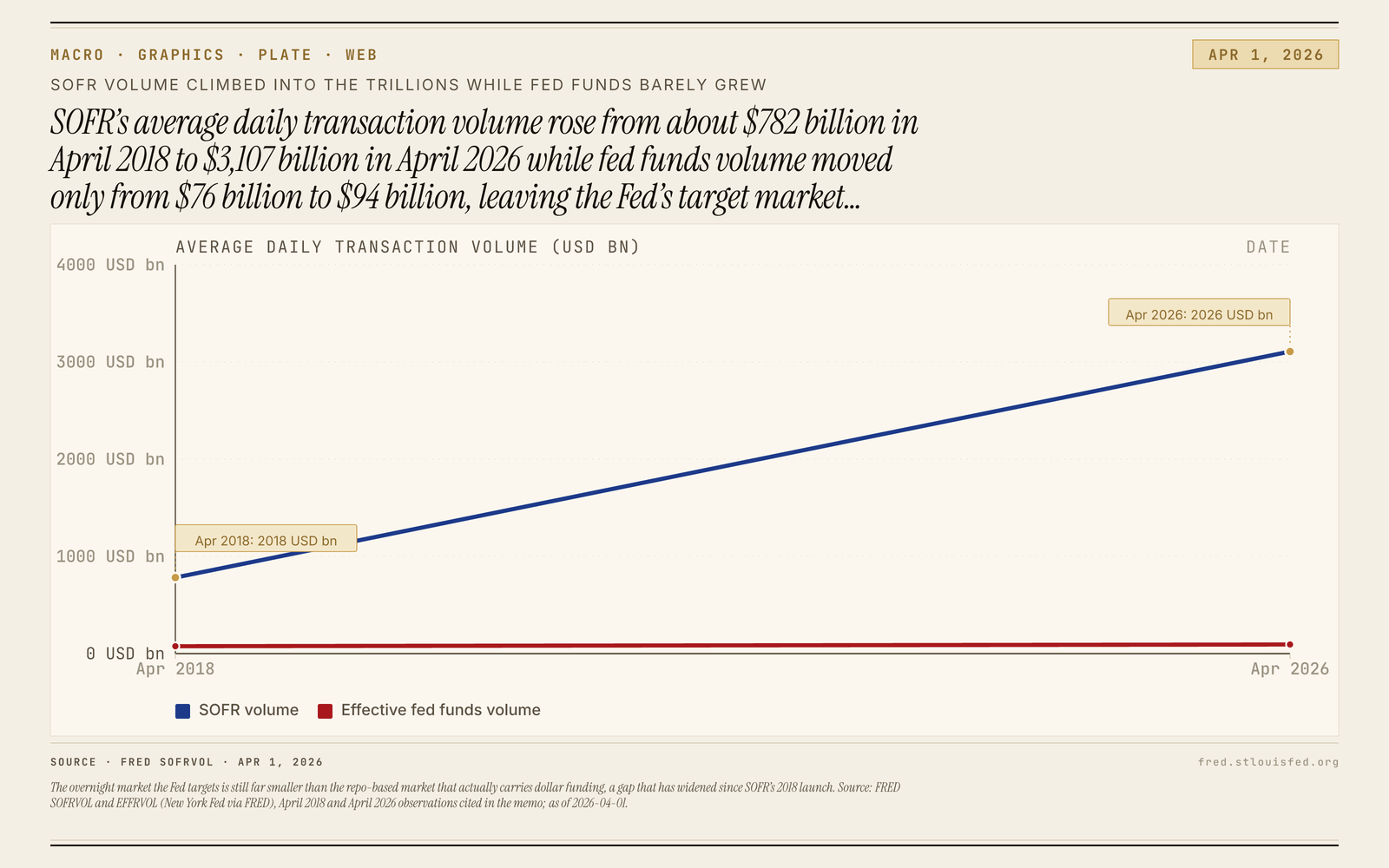

Plate 05SOFR Volume Towers Over Fed Funds

The chart shows SOFR far above fed funds in average daily transaction volume, from $782 billion versus $76 billion at the chart’s opening April average to $3,107 billion versus $94 billion at its latest April average, using New York Fed data via FRED (fred.stlouisfed.org ; fred.stlouisfed.org).

Plate 04

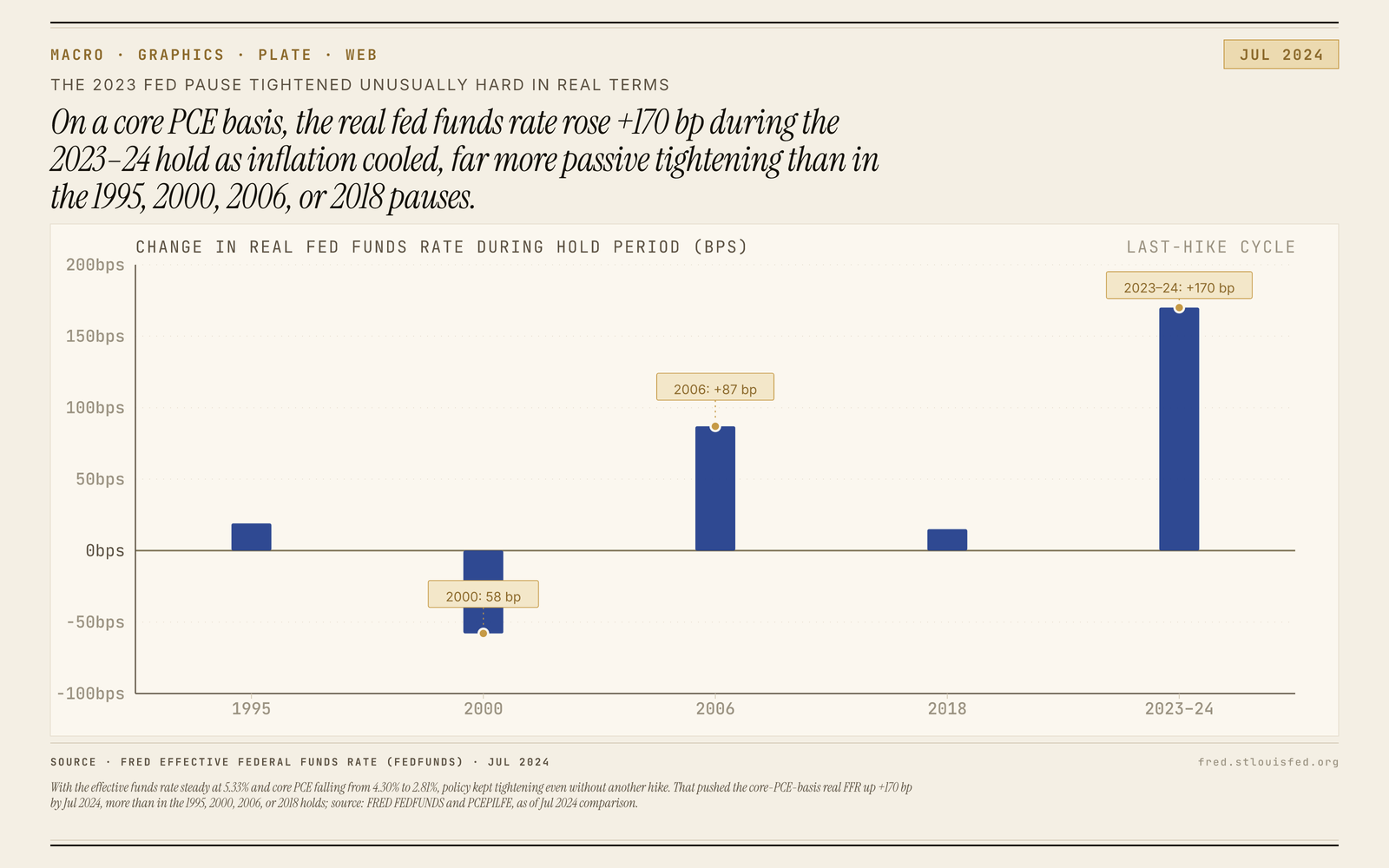

Plate 04Fed pause kept tightening in real terms

The chart shows the real fed funds rate climbing during the latest hold as inflation cooled, with the effective rate at 5.33% and core PCE falling from 4.30% to 2.81%.

Plate 03

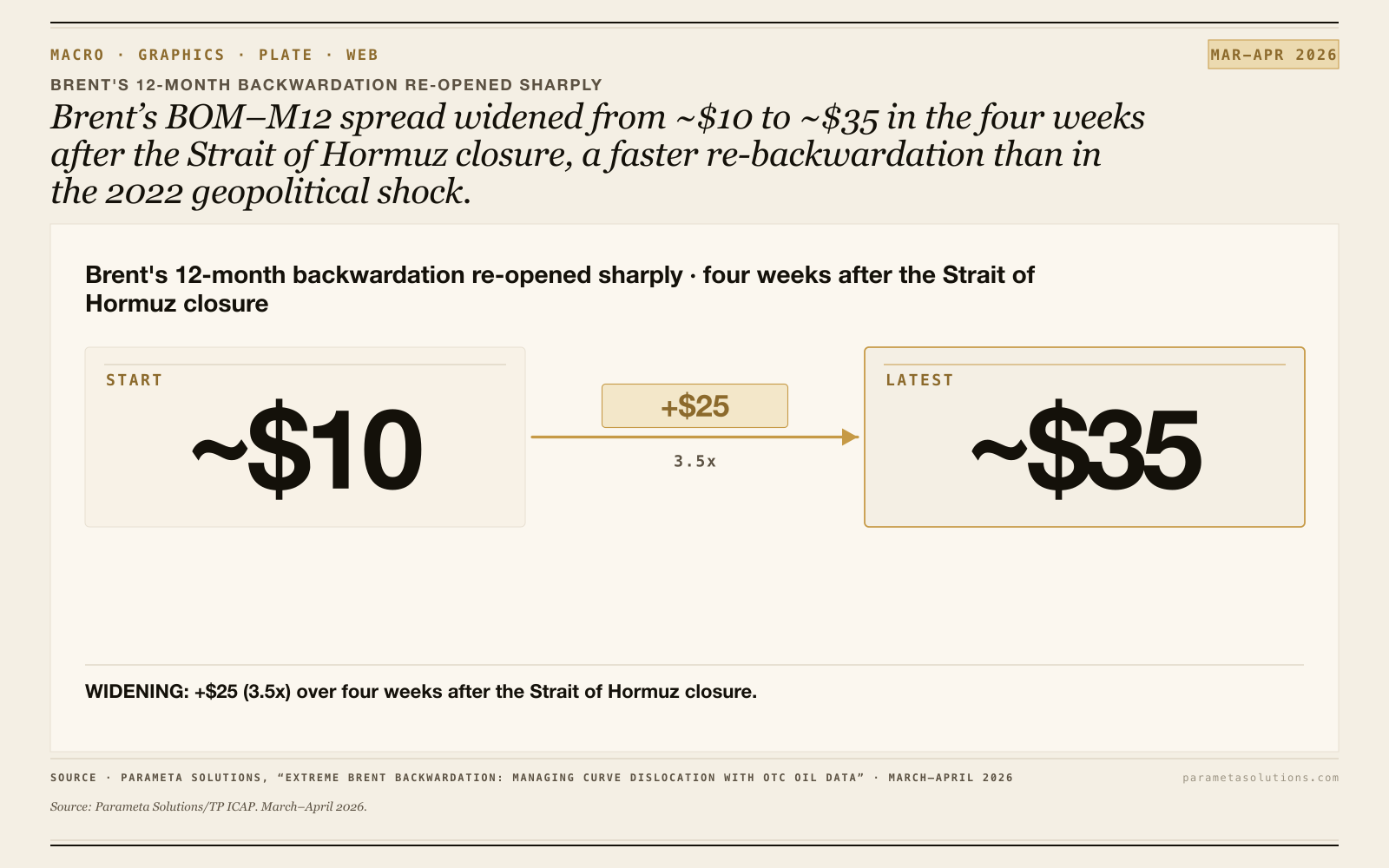

Plate 03Brent Front-End Re-Steepened by Apr. 10

Parameta's public April 10 note shows Brent's BOM-M12 spread moving from about $10 in early March to about $35 by April 10.

Plate 02

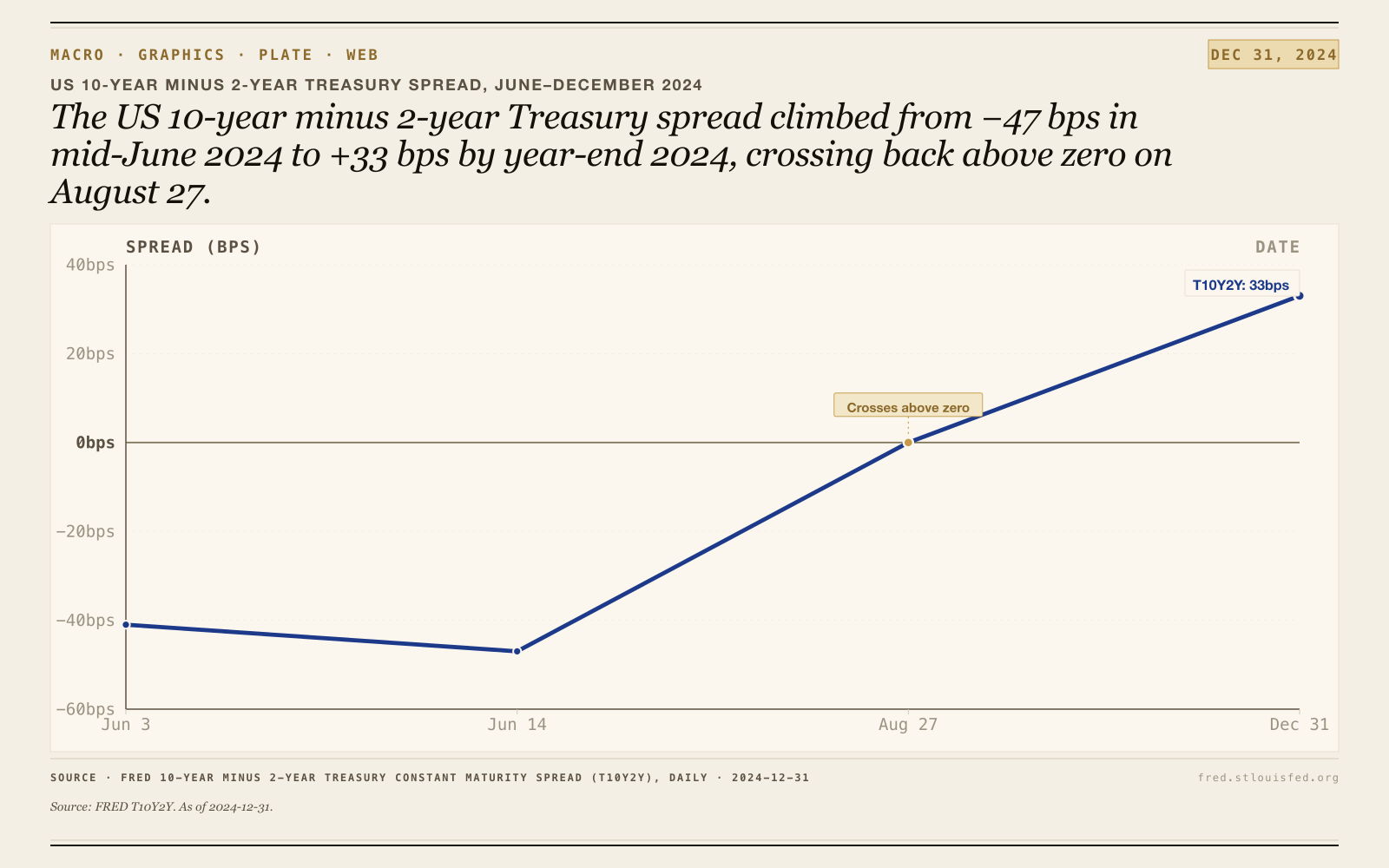

Plate 02Treasury spread turns positive again

The spread moved from −47 bps on 2024-06-14 to 0.00 bps on 2024-08-27 and finished at +33 bps on 2024-12-31.

Plate 01

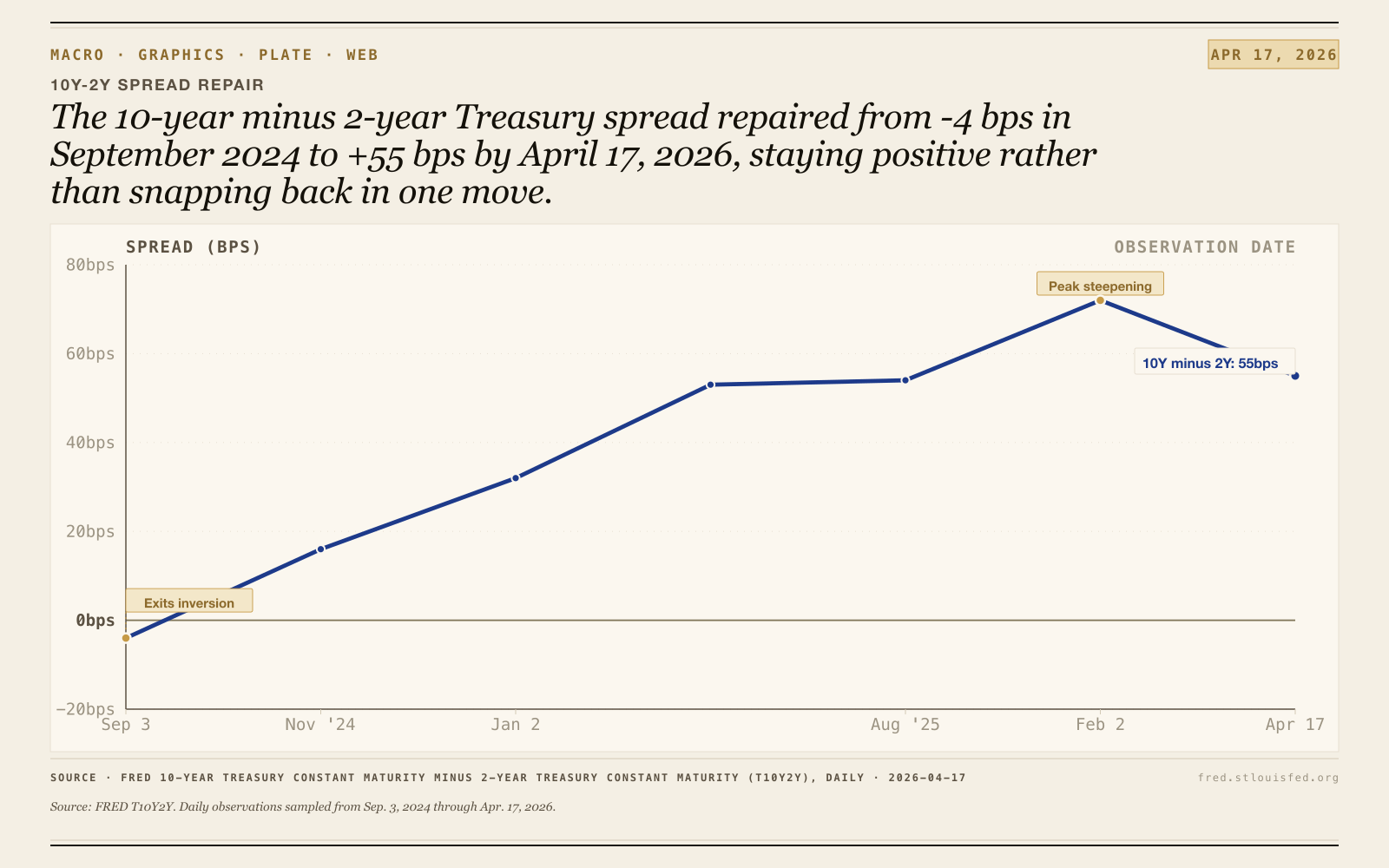

Plate 0110-Year minus 2-Year spread climbs higher

The 10-Year minus 2-Year Treasury spread is climbing higher in recent months, and the chart reads less like a snapback than a patient repair.